Burial Insurance

Burial life insurance, also known as funeral or final expense life insurance, refers to a whole life insurance policy that is designed for end-of-life expenses.

Do you need burial insurance?

Likely, yes.

Death is unavoidable, unfortunately. If you require funds to pay for bills accumulated upon your death, a burial policy is an excellent option.

The good news is this type of policy is easy to qualify for.

We will break down everything you need to know about burial life insurance, including a complete overview, the purchasing process and frequently asked questions – so that you can make an informed decision.

Table Of Contents

Burial Insurance Overview

Here, we’ll cover the primary features and functions of burial, or final expense, insurance.

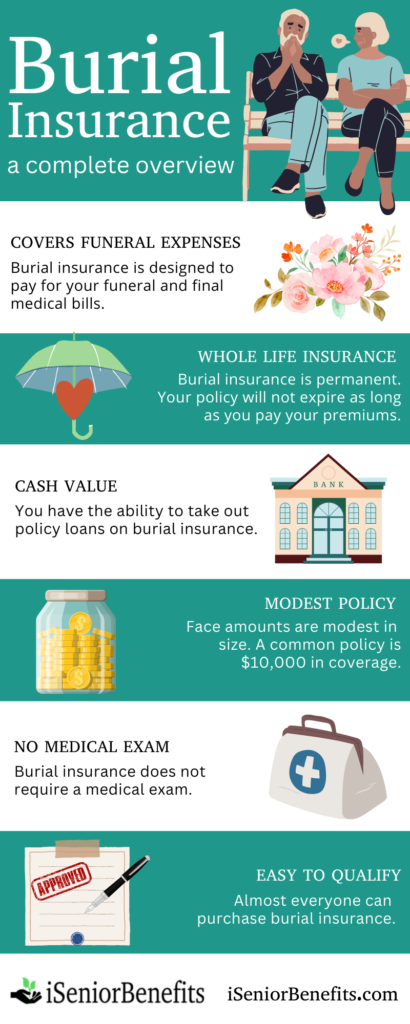

Policy Covers Funeral Expenses

Aptly named, burial insurance is primarily used as a means for loved ones to cover the price of your funeral and final medical bills.

- Casket or cremation

- Flowers

- Funeral service

- Hospital and nursing home bills

- Hospice

Burial Insurance Is Whole Life Insurance

It is important to know that burial insurance is a form of whole life insurance. In other words, you do not need to worry about outliving your life insurance policy.

Your policy never expires.

As long as you pay your premiums, your loved ones will receive a death benefit, regardless of when you pass away.

Cash Value Accumulates

Further, whole life insurance policies accumulate cash value. This means that you may borrow against your policy while you are still living.

Cash value does take time to build, and any unpaid balances at the time of your passing reduce the death benefit accordingly.

Modest Face Amounts

Designed to cover funeral costs and not much more, burial insurance policies are modest in size. As such, the cost of burial insurance is typically quite affordable.

Generally speaking, face amounts range from $2,000 – $40,000. Some carriers offer up to $50,000 in coverage.

However, the typical burial insurance policy is somewhere around $10,000 in death benefits.

To compare, the average funeral, which keeps increasing in price annually, will likely cost you somewhere between $7,000 – $12,000.

If you are in need of a larger policy to cover a mortgage, major debts, or to protect the financial livelihood of those who depend on you, a traditional life insurance policy makes more sense.

However, traditional coverage, like fully underwritten term or whole life insurance, is harder to qualify for and premiums are more expensive.

It’s important to remember that some coverage, like burial insurance, is better than no coverage, depending on your health and pocketbook.

No Medical Exam

Burial insurance does not require a medical exam. That means you skip the needles and nurses. Specifically, you will avoid providing liquid samples, blood pressure cuffs, and standing on a scale.

Because underwriting, the process of risk assessment on your life insurance application, is simplified, same-day approval happens all the time.

Easy To Qualify

Unlike traditional life insurance, burial life insurance utilizes a lenient underwriting process. In fact, the entire purchasing process is typically completed in one day.

Different types of burial insurance exist. Most, but not all, will require you to answer a few health questions and none will require a medical exam.

In other words, even if you are experiencing some medical problems, a burial policy is still an option for you.

There are two primary types of burial insurance:

- Simplified issue – some health questions.

- Guaranteed issue – no health questions.

You should know that the best option for most people is to purchase a policy that includes some health questions, known as simplified issue. Why? By answering those questions, you will pay less money for more coverage – and coverage begins right away.

Carriers utilize “knockout” health questions, similar to the following, for simplified issue policies:

- Are you hospitalized, receiving hospice, or living in a nursing facility?

- Have you been diagnosed with a terminal illness (for example, cancer)?

- Has a physician advised you to receive an organ transplant or an amputation?

- Have you been diagnosed by a physician as having AIDS or as HIV positive?

Note – each life insurance company’s specific burial insurance health questions vary.

On the other hand, if you have been diagnosed with a terminal illness, live in a nursing home, or can’t pass other knockout health questions, a guaranteed issue policy is always available.

A guaranteed issue policy should not be your first choice. Opt for a simplified issue policy if you can qualify.

Keep in mind, guaranteed issue life insurance always includes a waiting period. In other words, you will need to live for 2-3 years after the purchase of your coverage before your loved ones will receive the entirety of a policy’s proceeds.

How To Buy

Burial insurance is one of the simplest forms of coverage to purchase. Expect a straightforward process when applying.

Before you do anything else, enlist the help of an independent agent who specializes in burial insurance for seniors. That way, you have someone sitting on the same side of the table as you, so-to-speak.

Your independent agent will access multiple top-rated burial insurance carriers and walk you through the buying process, from start to finish.

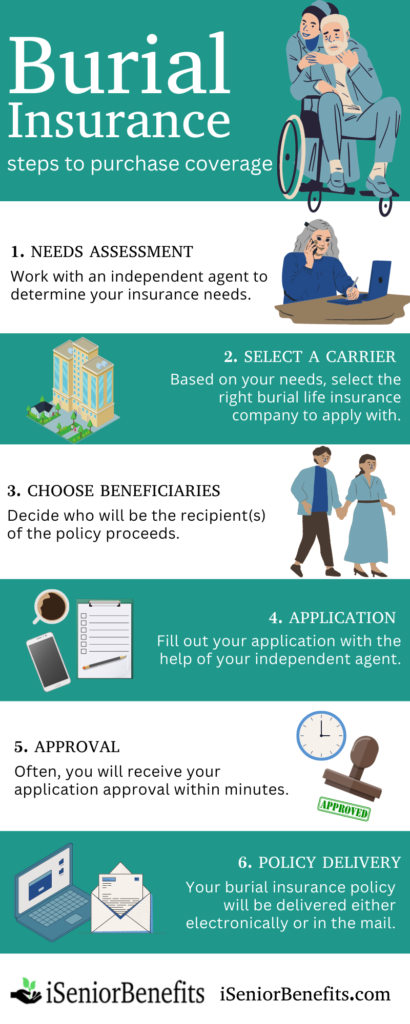

1. Needs Assessment

First, work with an independent agent to establish your burial insurance needs.

Grab a pen and paper, and jot down answers to the following:

- Funeral plans and associated costs.

- Balance of outstanding medical, hospital, hospice bills.

- Any other outstanding debts, such as credit card.

- Desire to leave a financial gift to a loved one.

- Intent to donate to a charity, church, or scholarship.

Your answers give you a general idea of what face amount, or policy size, you should purchase. Remember, burial insurance typically ranges from $2,000 – $50,000 in coverage.

2. Carrier Selection

Based on your monetary needs, and current health status, select a life insurance company to apply with. Again, an independent agent compares and contrasts your needs with the best carriers.

Be sure to evaluate highly regarded burial insurance carriers.

There are special circumstances that may influence the company you select. Be sure to let your agent know if either of the following apply to you:

- Military veteran status.

- Disabled status.

With the help of your agent, underwriting practices, premium cost, and policy details are closely assessed so that you find the best policy to match your needs.

3. Choose Beneficiaries

Your beneficiary is the recipient of your life insurance proceeds. At the time of your death, your beneficiary contacts the insurance company to file a claim and provide a death certificate.

Typically, beneficiaries are those you care most about, such as a spouse or child.

Eventually, communicate to your beneficiary where your policy is stored. That way, there are no delays when it comes time to file a life insurance death claim.

4. Complete Application

Burial insurance applications only take minutes to complete. You do not need to leave the comfort of your home as the entire process is usually completed over the phone.

Your specific application depends on the carrier, and whether you are applying for a simplified issue or guaranteed issue policy. Simplified issue includes basic health questions – guaranteed issue does not.

Plan to communicate the following basic information:

- Full name.

- Physical address.

- Date of birth.

- Gender.

- Social Security number.

- Desired coverage amount.

- Health information.

- Beneficiary details.

Pertaining to coverage amount, be sure to select a policy size that will cover all of your end-of-life costs, while still fitting into your budget. For example, many seniors buy a $10,000 burial policy.

Often, applications are approved and issued on-the-spot. Sometimes, further information is required by the underwriting team, but expect a quick turnaround.

Regardless of which type of application you fill out, it never includes a medical exam.

5. Application Decision

Often, you will receive an application decision within minutes because underwriting is straightforward.

Or, if your underwriter needs to confirm health information, as might be the case with a simplified issue policy, a few days of waiting is not out of the ordinary.

Just know that burial insurance has one of the fastest turnaround times out of all forms of insurance.

6. Policy Delivery and Review

Your policy will be delivered to you electronically, in the mail, or both.

Be sure to store your life insurance contract in a safe place. Communicate to your beneficiary where your burial policy is kept, so that it is easily accessed for a death claim.

Finally, be sure to carefully review your policy often. Life changes and you will want to make sure that your policy proceeds are going to those who will be in charge of your end-of-life care.

Think of it this way. Grief won’t be coupled with financial burden. Your policy will give your loved ones peace of mind, knowing that they will have the necessary financial resources to pay for the costs associated with your funeral and final bills.

Best Burial Insurance Companies

Many carriers offer burial insurance. Be sure to compare and contrast company features before applying.

There are five life insurance companies that are recommended after careful evaluation of:

- Customer service

- Ease of application and underwriting

- Affordability of premiums

- Policy features

- Company reputation

SBLI Living Legacy

SBLI, the “No Nonsense Life Insurance Company”, has been in business since 1907 and is based out of Woburn, Massachusetts. Founded by Louis Brandeis, an eventual Supreme Court Justice, SBLI insures over one million families nationally.

A.M. Best rating: A- (Excellent)

SBLI policy details at a glance:

- Ages: 50 – 85

- Minimum death benefit: $2,500

- Maximum death benefit up to age 75: $35,000

- Maximum death benefit ages 76 – 85: $20,000

- Riders included: LegacyShield – a free subscription to online tools, including a will, power of attorney, and advance directives

- Tobacco and non-tobacco premium rates

- Level benefit for Preferred and Standard health classes

- Modified benefit for those with serious health risks

Of note – SBLI’s unique partnership with LegacyShield helps prepare and organize important documents in one place. Final wishes, family photos, an estate plan, a will, power of attorney, financial accounts, and advanced directives are all included

Important – also included with each SBLI burial insurance policy is the Sequoia Funeral Concierge Plan, a highly beneficial program designed to assist in all funeral planning aspects.

Bottom line – the application is an instant decision process with only a few health questions asked, meaning that you will immediately know if you have been approved for the policy.

American Amicable Senior Choice

Founded in 1910, and based out of Waco, Texas, American Amicable’s history of providing exceptional life insurance products is impressive.

A.M. Best rating: A (Excellent)

American Amicable policy details at a glance:

- Ages: 50 – 85

- Minimum death benefit: $2,500 ($5,000 in WA)

- Maximum death benefit up to age 75: $50,000

- Maximum death benefit ages 76 – 85: $25,000

- Riders included: Terminal Illness, Confined Care

- Optional riders: Grandchild, Nursing Home Waiver of Premium, Children’s Insurance Agreement, Accidental Death

- Tobacco and non-tobacco premium rates

- Level benefit for Preferred and Standard health classes

- Modified benefit for those with serious health risks

Of note – tobacco users receive favorable rates and their height/weight charts are liberal.

Bottom line – there are three plans available through American Amicable’s Senior Choice product: Immediate Benefit, Graded Benefit, and Return of Premium. Your health status determines which plan you qualify for.

Prosperity PrimeTerm to 100

Founded in 2009, Prosperity Life Insurance Group is headquartered in Austin, TX. They have a number of member companies, including:

- Shenandoah Life Insurance Company

- SBLI Life Insurance Company, Inc.

- S. USA Life Insurance Company

Prosperity policy details at a glance:

- Ages: 40 – 80

- Minimum death benefit: $5,000

- Maximum death benefit: $30,000

- Rider included: Accelerated Death

- Optional rider: Accidental Death

- Graded death benefit for the first two policy years

- Only three health questions

Of note – the initial term is for 20 years. A decreasing death benefit lasts until age 100.

Bottom line – Prosperity PrimeTerm to 100 offers coverage starting at age 40 and applicants can be approved right away by answering only three health questions.

Guarantee Trust Life Heritage Plan

Headquartered in Glenview, IL, Guarantee Trust Life (GTL) was founded in 1936. The carrier is a family-run company. In fact, President Richard S. Holson III is the third family member to hold office.

A.M. Best rating: A- (Excellent)

Guarantee Trust Life policy details at a glance:

- Ages: 40 – 90.

- Minimum death benefit: $2,500.

- Maximum death benefit: $25,000.

- Riders included: temporary Accidental Death Benefit (for first two years).

- A Suicide Exclusion exists (for the first two years).

- Policy benefits are always graded (except for accidental death).

- Only five health questions.

Of note – the entire purchasing process is completed online with a corresponding telephone signature. No paper applications are available. GTL issues coverage up to 90 years old (most carriers stop issuing coverage at 80 – 85 years).

Important – Guarantee Trust Life now offers free enrollment into the Sequoia Funeral Concierge Plan with a Heritage Plan purchase, a highly beneficial program designed to assist in all funeral planning aspects.

Bottom line – GTL’s simple application with only five health questions will provide you with an accept/reject answer on the spot. No further underwriting will ever be required.

CICA Life Superior Choice

CICA Life, a subsidiary of Citizens Inc., was incorporated in Texas in 1965. CICA Life of America is licensed in many states nationwide and utilizes Citizens Inc. to bring innovative technology and operations to their company.

A.M. Best rating B++ (Good)

CICA Life Super Choice policy details at a glance:

- Ages: 0 – 85

- Minimum death benefit: $1,000

- Maximum death benefit up to age 70: $30,000

- Maximum death benefit up to age 85: $10,000

- Riders included: Terminal Illness, Dismemberment

- Optional riders: Accidental Death

- Level benefit for Standard

- Graded benefit for Guaranteed Issue

- Not available in the following states CA, NY

Important – CICA Life Superior Choice does not ask height, weight or tobacco use questions.

Corebridge Guaranteed Issue Whole Life

Formerly AIG, Corebridge Financial was originally rooted in Shanghai in 1919 by Cornelius Vander Starr. Today, Corebridge operates in more than 70 countries and millions of Americans use their insurance products.

A.M. Best rating: A (Excellent)

Corebridge GIWL policy details at a glance:

- Ages: 50 – 80

- Minimum death benefit: $5,000

- Maximum death benefit: $25,000

- Riders included: Accelerated Death Benefit

- Policy benefits are always graded (except for accidental death)

- Everyone qualifies

Of note – because the policy is guaranteed to be issued, premiums are more expensive than other forms of burial insurance.

Bottom line – if you are in poor health and cannot qualify for other coverage, Corebridge’s guaranteed issue life insurance is a godsend. However, if you can qualify for a simplified issue policy with a few health questions, look there instead.

Mutual of Omaha Living Promise

Originally named Mutual Benefit Health and Accident Association, Mutual of Omaha was founded in 1909 by a medical student, Dr. Criss, attending Creighton University. Today, Mutual of Omaha is a Fortune 500 company and offers a multitude of insurance and financial products.

A.M. Best rating: A+ (Superior)

Mutual of Omaha policy details at a glance:

- Ages: 45 – 85

- Minimum death benefit: $2,000 ($5,000 in WA)

- Maximum death benefit: $40,000

- Riders included: Accelerated Death Benefit for Terminal Illness or Nursing Home Confinement (level benefit plan only and varies by State)

- Optional rider: Accidental Death Benefit

- Tobacco and non-tobacco premium rates

- Level benefit and graded (modified) benefit depending on health status

- Graded benefit is not available in AR, MT, NC or WA

Of note – Mutual of Omaha is one of the top-rated life insurance carriers on the market.

Bottom line – premium rates are very affordable for their level benefit policy, if you can qualify.

Frequently Asked Questions

Consider the following frequently asked questions when deciding if burial insurance is right for you.

How much will burial insurance cost?

Burial insurance policies are affordable, primarily because the death benefit is modest compared to other forms of life insurance.

There are a number of primary factors that affect the cost of burial insurance:

- Age

- Gender

- Policy face amount

- Health

- Tobacco use

Here are two examples, based on the average burial policy of $10,000:

- 65 year old average health female, non-smoker: $42.80/mo.

- 75 year old poor health male, smoker: $85.16/mo.

What is the average cost of a funeral?

$7,000 – $12,000

However, the price of a funeral vary by state. Further, the costs of funerals are increasing annually.

Costs include a funeral service, casket or urn, embalming or cremation, flowers, obituary, grave marker and headstone.

Keep in mind, most individuals have final medical bills in addition to the cost of a funeral.

Should I buy a burial life insurance policy?

Probably.

Consider purchasing a policy if… you wish to cover your funeral and burial expenses at least so that your assets remain intact for your legacy and heirs.

– Insurance Information Institute

The truth is, no one gets out of here alive. If you are in need of funds to cover bills when you pass away, burial insurance is worth it.

Will my policy ever expire?

No.

As long as you make your premium payments, your policy will not expire. Burial insurance is almost always permanent.

Will my burial insurance have a waiting period?

It depends.

If you are approved for a simplified issue burial policy, with level benefits, you may not have a waiting period.

However, many burial insurance policies are graded – due to an applicant’s answers to the health and lifestyle questions on the application. A graded policy typically requires two years of waiting before the full death benefit will be paid.

During the first two policy years, if the insured passes away, usually premiums, plus interest, are returned.

Note – guaranteed issue life insurance plans always have a waiting period.

Who should I list as my beneficiary?

Generally-speaking, your life insurance proceeds should be intended for anyone whose financial livelihood depends on you.

One of the greatest gifts my father ever gave me was help planning his very own death. About a month or two before he died, he sat me down at the kitchen table and he helped me make a list of everything I needed to do once he was gone.

Remembering a Life

Specific to burial insurance, it makes sense to name the person who will be responsible for your end-of-life finances, such as a spouse or child.

Do I have to use my policy on burial expenses?

No.

In fact, the death benefit of your policy can be used in any way you see fit.

Perhaps your loved ones need funds to:

- Pay off credit card debt.

- Start a college fund for grandchildren.

- Make a donation to a charity or church in your honor.

- Cover loan payments.

The beneficiary to your burial insurance policy will receive the death benefit as a lump sum (almost always) and they may use the funds as they best see fit.

Next Steps

Seniors deserve to have peace of mind knowing that funds are in place to cover their end-of-life expenses.

Fortunately, iSeniorBenefits was established to do exactly that – provide a one-stop shop for all of your burial insurance needs.

Secure high quality, affordable burial insurance today by taking advantage of iSeniorBenefits’ comprehensive range of insurance options designed specifically for the senior population.