Cancer Plans

Statistics surrounding cancer diagnoses in the United States are sobering.

The lifetime risk of developing cancer:

- Men have one-in-two odds.

- Women have slightly more than one-in-three odds.

Chances are, you know family and friends who have been diagnosed with the serious disease.

The good news is that cancer survival rates have drastically increased over the decades, thanks to impressive advancements in treatments. The bad news is that the cost of cancer therapeutics can best be described as astronomical.

Should you find yourself with the C-word, one of the first things you will want to do is confirm that you have funds available to cover expensive treatment options and secure excellent care. Often, a cancer plan is a key component.

Further, most cancer insurance plans include the option to add coverage for heart attacks and strokes.

Combined, you have the ability to secure financial protection for three leading causes of serious illnesses in the United States – without needing to dig into your savings to do so.

This is your go-to guide for cancer, heart attack and stroke insurance. You will learn about your insurance options, the importance of coverage, and frequently asked questions.

Table Of Contents

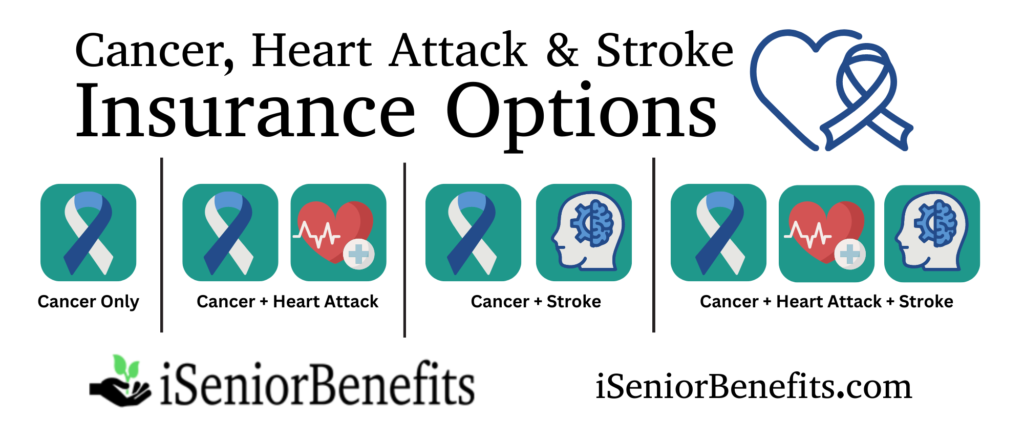

Options For Cancer Plans

Many cancer insurance plans exist, each with their own specific features. What you can count on is finding insurance protection to fit your needs and budget.

Generally speaking, you may select cancer protection only, or varying combinations of cancer, heart attack and stroke coverage.

- Cancer only

- Cancer and heart attack

- Cancer and stroke

- Cancer, heart attack, and stroke

Further, cancer insurance can be used in conjunction with another health insurance plan you may have.

While specific attributes of a cancer plan vary by carrier, you can expect options similar to the following.

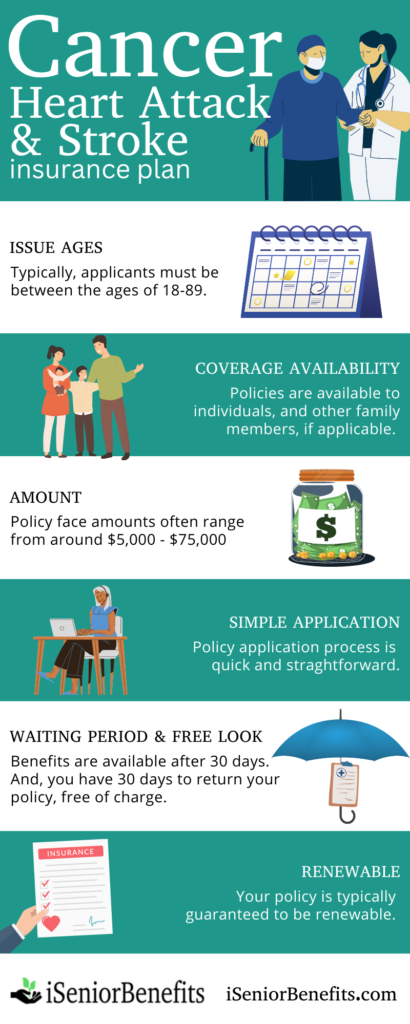

Issue Ages

Most cancer plans issue coverage to individuals between the ages of 18 – 89, thankfully allowing almost all adults in the United States the opportunity to purchase insurance.

Coverage Availability

Plans are available not just for the individual, but under all of the following circumstances:

- Individual

- Individual and spouse/domestic partner

- Individual and children

- Family

That way, you have the option to extend coverage to those you care most about.

Face Amount

You have the ability to select from a wide range of policy face amounts, usually between $5,000 – $75,000.

When considering what size of policy to purchase, evaluate the following. Keep in mind, your coverage can pay for costs beyond medical treatment, known as indirect costs.

- Therapeutics and medical care

- Transportation

- Loss of work income

- Counseling

- Hotel and lodging expenses

- Living expenses

Simple Application

You can expect a quick straightforward application process, often completed online or over the phone.

Plan to provide information about the following:

- Whether the application is new, a reinstatement, a benefit increase, or for an additional dependent.

- Your basic information, including social security number, full name, height, weight, gender, address, contact information.

- Primary physician’s contact information.

- If applicable, additional dependent’s social security number, gender, date of birth, height and weight.

- Whether you are applying for cancer coverage only, or a combination of cancer, heart attack and/or stroke coverage.

- Whether you or your dependents have ever been denied insurance for health reasons.

- If anyone applying for coverage has ever been diagnosed with Acquired Immune Deficiency (AIDS) or a related condition.

- Whether you or your spouse are pregnant.

- If the coverage is intended to replace another policy that is currently in force.

An independent agent will walk you through the application process and verify you are applying with a carrier that meets your needs.

Waiting Period And Free Look

You should know that most cancer plans require a 30-day waiting period. This means that your benefits will not be available until 30 days after the policy is in force.

Why? A waiting period is a protective mechanism for carriers.

It safeguards a company from someone filing a claim immediately upon coverage approval, which typically indicates the insured knew of an existing medical condition prior to the coverage approval.

Further, you are entitled to a free look period of typically 30 days. If, for any reason, you determine that the policy does not fit your needs or you no longer want the coverage, you can return the plan at no cost to you.

Renewable Coverage

Many cancer plans are guaranteed to be renewable. You can have peace of mind knowing that your plan cannot be canceled. As long as you make your premium payments, your policy will stay in force.

Exclusions and Limitations

Circumstances exist in which cancer, heart attack, and stroke insurance either limits or excludes coverage.

While the plans are generally comprehensive, you do need to be aware of conditions in which a loss will not be paid for.

For example, typically the following situations are excluded or limited.

Cancer

Losses resulting from:

- Intentional self-inflicted injury or sickness.

- Unless prescribed by your doctor, use of drugs or other intoxicants.

- Exposure to a declared or undeclared war, or any act pertaining to war.

Illnesses and conditions:

- Skin cancer, other than malignant melanoma.

- Premalignant conditions or health conditions with a malignant potential.

- Any disease or illness other than cancer, even if the disease or illness was complicated or aggravated as a result of cancer.

Heart Attack Or Stroke

Losses resulting from:

- Suicide or any attempt at suicide, or any attempt at self-inflicted injury or illness.

- Unless prescribed by your doctor, use of drugs or other intoxicants.

- Commission or attempted commission of a felony in which the insured person was engaged in an illegal occupation.

- Voluntary participation in a riot or civil insurrection.

- Exposure to a declared or undeclared war, or any act pertaining to war.

- Balloon angioplasty procedure, laser relief, or similar procedure.

Illnesses and conditions:

- Transient Ischemic Attack (TIA)

- Brain damage as a result of an accident or injury, infection, vasculitis, inflammatory disease, or demyelinating process.

- Vascular disease affecting the eye or optic nerve.

- Vertebrobasilar insufficiencies.

- Incidental imaging findings.

- Ischemic disorders of the vestibular system.

- Disease or injury of the cardiovascular system other than heart attack.

- A cardiac arrest not caused by heart attack.

- Any diseases or illnesses other than heart attack or stroke, even if the disease or illness was complicated or aggravated as a result of heart attack or stroke.

Importance Of Coverage

Rates of cancer diagnoses, heart attacks, and strokes occurring in the United States are eye-opening. To get a general idea, consider the following key points related to how often diagnoses occur and, in particular, cost of care.

It’s not just the initial diagnosis or medical event that creates financial strain, rather, the long term treatment and recovery plan is usually when significant costs accrue.

Cancer

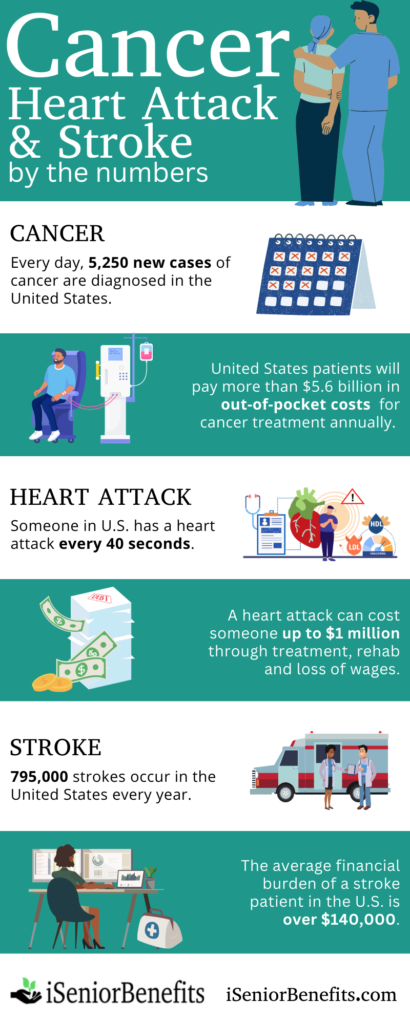

Every single day, there are, on average, 5,250 new cases of cancer diagnosed in the United States according to the American Cancer Society.

Cancer is defined as “a disease manifested by the presence of malignancy characterized by the uncontrolled growth and abnormal spread of malignant cells and the invasion of body tissue by such malignant cells”.

The most common forms of cancer include:

- Breast

- Prostate

- Lung

- Colon

- Melanoma of the skin

- Urinary bladder

In total, these prevalent cancers are estimated to have well over one million new cases on an annual basis.

Further, the costs associated with cancer treatment are pushing many American families into debt. While advances in care are impressive and rates of recovery increase every year, the cost burden has risen alongside the improvement in oncology therapeutics.

About two-thirds of adults with health care debt, who’ve had cancer themselves or in their family, have cut spending on food, clothing, or other household basics.

Kaiser Family Foundation

Just like typical health insurance does not cover, dental, vision and hearing insurance, a separate plan is often needed for extensive cancer coverage, as well.

And, it’s not just the medical treatment that becomes expensive. Called indirect expenses, the bills associated with transportation, lodging, loss of wages, and general rehabilitation adds up quickly.

The American Cancer Society’s Action Network details just how deep invoices run for cancer patients. Astonishingly, the typical out of pocket costs Americans face is over $5.6 billion yearly.

Heart Attack

Someone in the United States has a heart attack every 40 seconds.

Insurance companies define a heart attack as an “acute myocardial infarction resulting in the death of a portion of the heart”.

Heart attacks sometimes cause complications as a result of damage to the heart muscle. According to the Mayo Clinic, your heart may experience the following after a heart attack:

- Irregular heart rhythms, also known as arrhythmias

- Cardiogenic shock

- Heart failure

- Inflammation of the saclike tissue around the heart (pericarditis)

- Cardiac arrest

Fortunately, most people can recover from a heart attack, especially with prompt treatment and appropriate rehabilitation.

While follow-up care is a necessary component to recuperating from a heart attack, the financial implications are astonishing. One heart attack can cost someone up to $1 million through treatment, rehabilitation, and loss of wages.

Stroke

795,000 strokes occur in the United States every year.

By definition, a stroke is an “acute cerebrovascular event caused by intracranial thrombosis or hemorrhage, or embolism from an extracranial source, with acute onset of new neurological symptoms”.

In other words, strokes occur when blood flow is unable to reach the brain, usually either from a blood clot or a ruptured blood vessel.

According to the American Stroke Association, there are four primary types of strokes:

- Ischemic (clots) – accounts for 87% of all strokes

- Hemorrhagic (bleeds)

- Cryptogenic

- Brain Stem

Note – Transient Ischemic Attacks (TIA) are often referred to as “mini strokes”, and should be treated as a warning sign. TIAs are typically not covered in stroke insurance.

The average costs associated the most common form of stroke, ischemic, is more than $140,000. This figure includes inpatient care and rehabilitation. The burden rises dramatically if loss of wages are calculated.

Frequently Asked Questions

Frequently asked questions about cancer plans and their important answers are found here.

Should I buy a cancer plan?

Possibly.

Know that the monetary stress of cancer, heart attacks and strokes are leading causes of medical bankruptcies.

Most health insurance plans do not offer comprehensive coverage, and doctor and hospital bills pile up quickly.

We recommend asking yourself, “Are the premium costs worth the peace of mind?”.

Further, some policies include a return-of-premium option in which your premium payments will be returned to you if you are not diagnosed with cancer.

What are some reasons I should buy a cancer plan?

Purchasing cancer coverage is a personal decision, and one that should be thought out carefully.

Seriously consider a cancer plan if any of the following relate to you:

- Family history of cancer, heart disease or stroke.

- Your health insurance lacks comprehensive coverage.

- You are without sufficient savings to cover the out-of-pocket costs of a major medical event.

What if I have already been diagnosed with cancer?

Work with an independent insurance agent.

They will assess your specific medical history and be able to determine if there is a plan available to you.

Not all carriers accept applicants with a history of certain types of cancer, or other serious medical conditions, like AIDS or Hodgkin’s disease.

Is a cancer plan a form of life insurance?

No.

Cancer insurance is a distinct form of health insurance.

Look into a life insurance policy, like burial insurance, to ensure that end-of-life expenses are taken care of and loved ones are not saddled with debt.

How To Buy

You can count on a quick and easy process for buying a cancer plan.

Remember, approval is not guaranteed, and you will want to compare and contrast different plan features.

The first thing you need to do is partner up with an independent agent so that you have access to multiple carriers. Captive agents can only represent the company that employs them.

Next, be prepared to answer the application questions. Expect general questions including your contact information, height and weight, any history of cancer, and information about other family members who will also be on the policy, if applicable.

Finally, your application is submitted and a decision is made by the carrier. Most people are approved for cancer, heart attack and/or stroke coverage.

Keep in mind – cancer plans are often guaranteed renewable. As long as you make your premium payments, you are promised to have coverage.